Welcome to our Market Update, written by our very own Capital Market experts. This blog is designed to give you a glance into the most important market events happening this week.

Market Commentary:

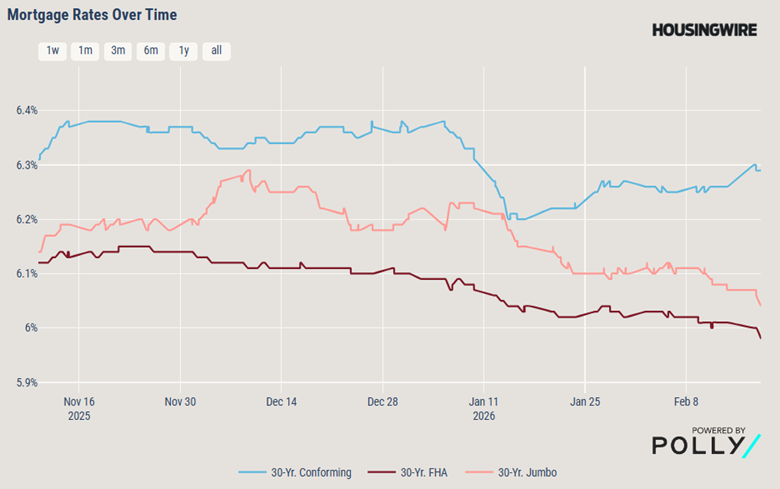

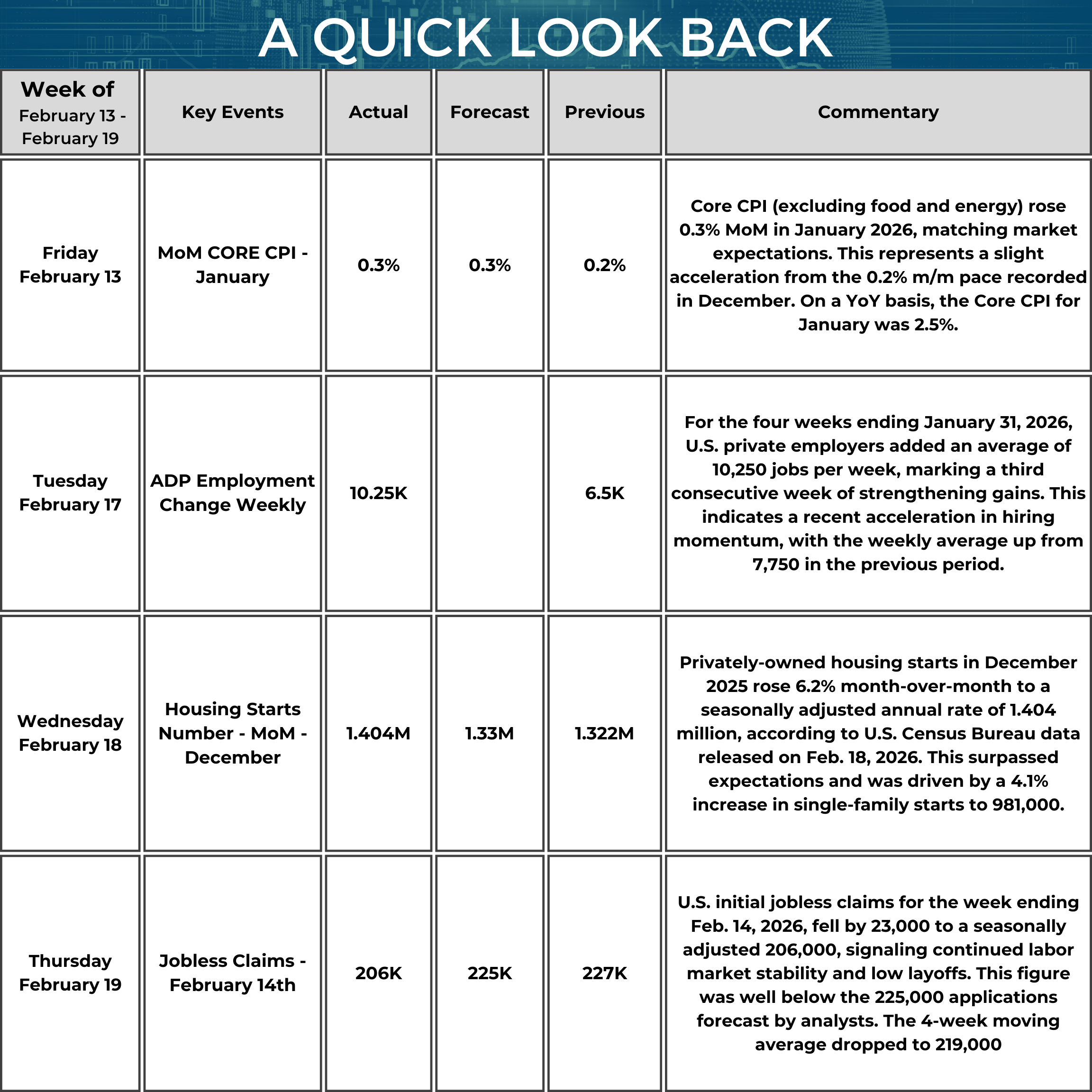

During the week of February 13–19, 2026, U.S. interest rate conditions were shaped primarily by moderating inflation indicators and renewed evidence of labor‑market strength. Collectively, these factors contributed to a stable but slightly reactive mortgage rate environment, with rates declining early in the week before experiencing modest upward pressure.

The week’s economic signals collectively pointed to a balanced interest‑rate environment in which inflation progress supported rate stability, while strong labor performance moderated expectations of near‑term monetary easing. As a result, mortgage markets experienced only marginal rate volatility, maintaining favorable conditions for both homebuyers and refinancing scenarios.

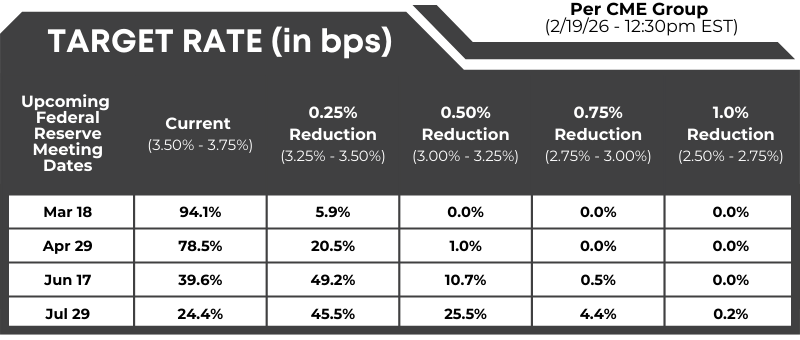

FedWatch: Target rate (in bps) possibilities, according to the CME Group (as of 02/19/2026 – 12:00 PM EST):

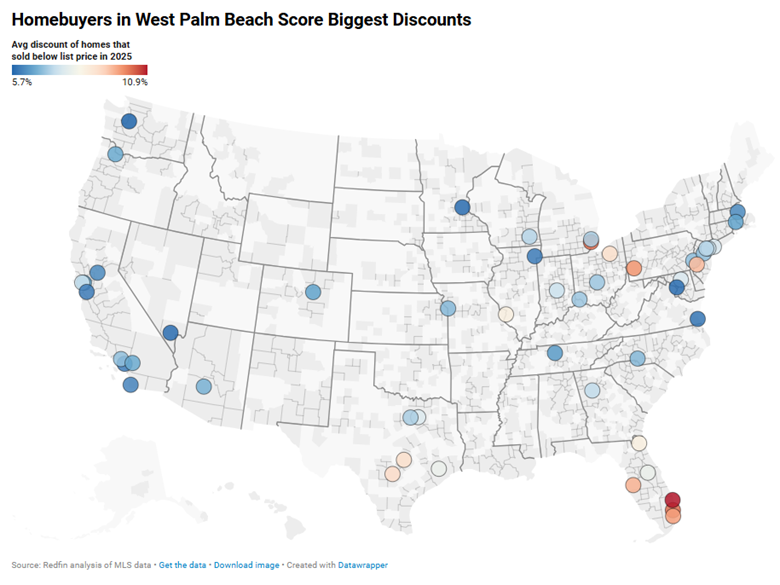

Homebuyers Are Scoring The Biggest Discounts in 13 Years:

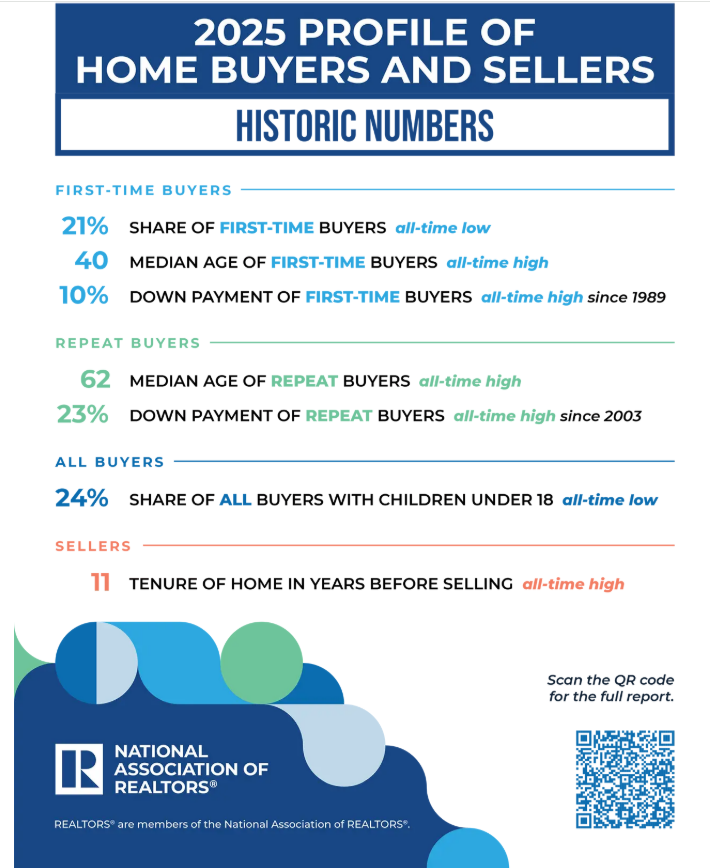

Highlights From the Profile of Home Buyers and Sellers

AI Activity:

AI is simultaneously creating pricing power and eroding it. In addition to the uncertainty surrounding future cash flows to the hyper scalers, LLMs are extending Big Tech’s dominance by automating and compressing margins for software as service providers (think Adobe, Salesforce...). But at the same time, hyper scaler AI demand is pushing up value where there are hard physical constraints and supply-chain bottlenecks including memory, energy infrastructure, energy storage, chips and more. - Elliot Eisenberg, Economist

News You Can Use:

· Fed minutes January 2026: Fed officials split on where interest rates should go, minutes say

· Mortgage rates sink to the lowest level in a month, sparking more refinance demand

· Federal Reserve Wants To Loosen Bank Rules To Boost Mortgage Lending

· 'On the right path': Housing market offers glimmers of hope, some analysts say -ABC News

· States With the Highest Property Taxes Revealed

· Builder Sentiment Edges Lower on Affordability Concerns | NAHB

· US December durable goods orders - 1.4% vs -2.0% expected | investingLive

*Communication is intended for Industry Professionals only and not intended for Consumer Distribution

Interest rate and annual percentage rate (APR) are based on current market conditions as of 02/19/2026, are for informational purposes only, are subject to change without notice and may be subject to pricing add-ons related to property type, loan amount, loan-to-value, credit score and other variables. Estimated closing costs used in the APR calculation are assumed to be paid by the borrower at closing. If the closing costs are financed, the loan, APR and payment amounts will be higher. Contact us for details. Additional loan programs may be available. Accuracy is not guaranteed, and all products may not be available in all borrower's geographical areas and are based on their individual situation. This is not a credit decision or a commitment to lend. Actual interest rate, APR, and payment may vary based on the specific terms of the loan selected, verification of information, your credit history, the location and type of property, and other factors as determined by Prosperity Home Mortgage, LLC. Not available in all states. Rate is as of 02/19/2026 and is subject to change at any time without notice. Opinions, estimates, forecasts, and other views contained in this document are those of Freddie Mac’s economists and other researchers, do not necessarily represent the views of Freddie Mac or its management, and should not be construed as indicating Freddie Mac’s business prospects or expected results. Although the authors attempt to provide reliable, useful information, they do not guarantee that the information or other content in this document is accurate, current, or suitable for any particular purpose. All content is subject to change without notice. All content is provided on an “as is” basis, with no warranties of any kind whatsoever. Information from this document may be used with proper attribution.