This Market Update is written by our Capital Market specialists each week to bring you insight into what's happening in the market and how it may affect mortgage rates and real estate trends.

Rates are provided by Housing Wire in conjunction with Polly. Rates are updated in real-time. Polly data is calculated using actual locked rates. Rates are inclusive of locks that occur below par, at par and therefore consider discounts and rebates.

Market Commentary:

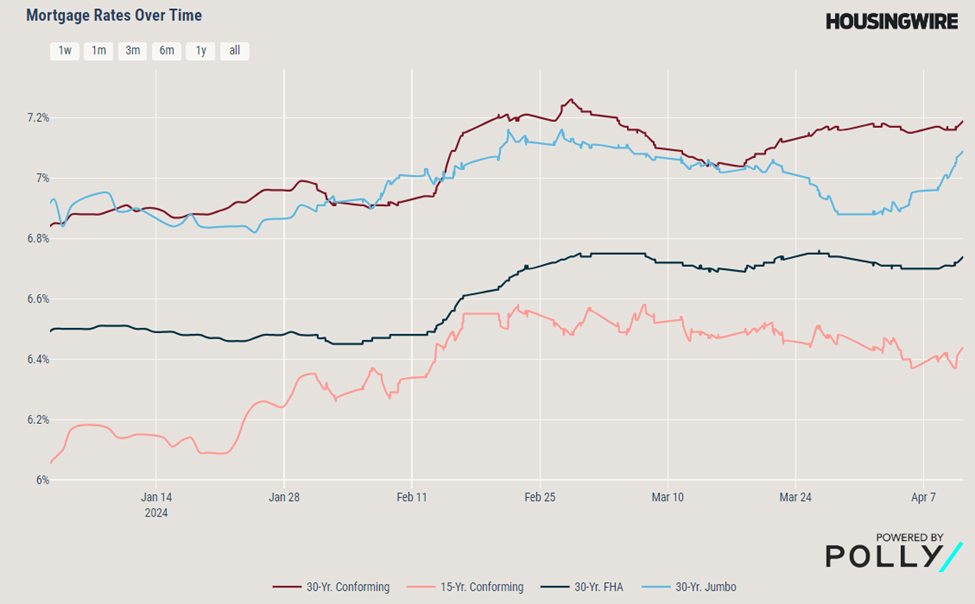

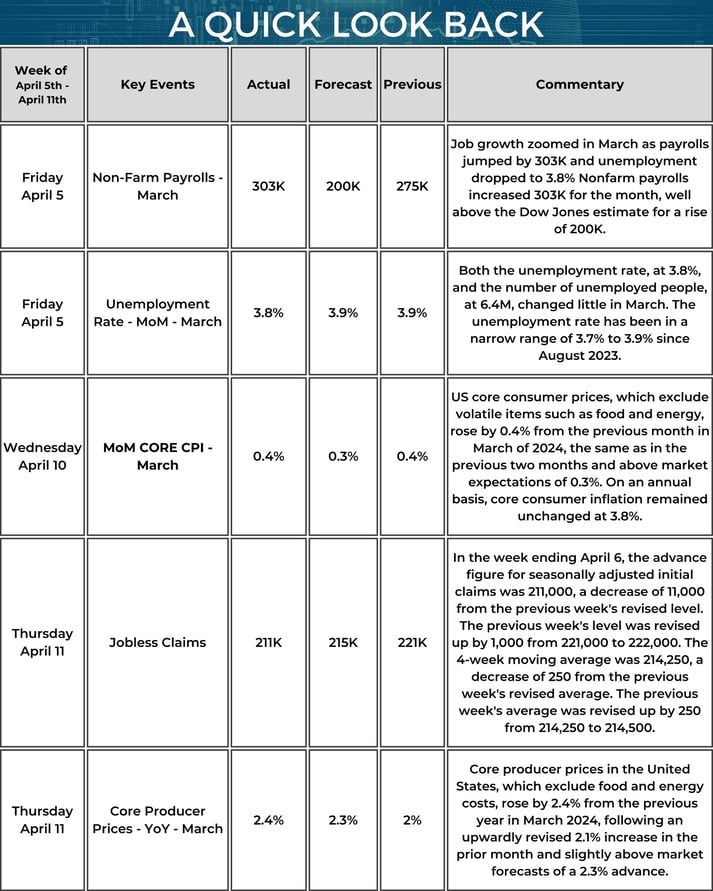

For the week of April 5th to April 11th, interest rates increased slightly due to higher than expected CPI numbers. Inflation’s decline is stalling and thus Fed rate relief remains on hold. The Fed is now forecasting two rate cuts in 2024 with the first move coming in July.

Fed Watch:

Target rate (in bps) possibilities, according to the CME Group:

|

Upcoming Federal Reserve Meeting Dates |

Current (5.25% - 5.50%) |

0.25% Reduction (5.00% - 5.25%) |

0.5% Reduction (4.75% - 5.00%) |

|

May 1st |

97.5% |

2.5% |

0% |

|

June 12th |

79.1% |

20.4% |

0.5% |

|

July 31st |

52.9% |

39.8% |

7.1% |

List of the 10 Metro Areas with Largest Share of Price Reductions of Total Inventory

-

Tampa-St. Petersburg-Clearwater, Fla. – 27.6%

-

Phoenix-Mesa-Chandler, Ariz. – 23.0%

-

Austin-Round Rock-Georgetown, Texas – 22.3%

-

Jacksonville, Fla. – 22.1%

-

San Antonio-New Braunfels, Texas – 21.8%

-

Orlando-Kissimmee-Sanford, Fla. – 20.2%

-

Portland-Vancouver-Hillsboro, Ore.-Wash. – 20.1%

-

Miami-Fort Lauderdale-Pompano Beach, Fla. – 19.7%

-

Dallas-Fort Worth-Arlington, Texas – 19.5%

-

Memphis, Tenn.-Miss.-Ark. – 19.3%

Market Review:

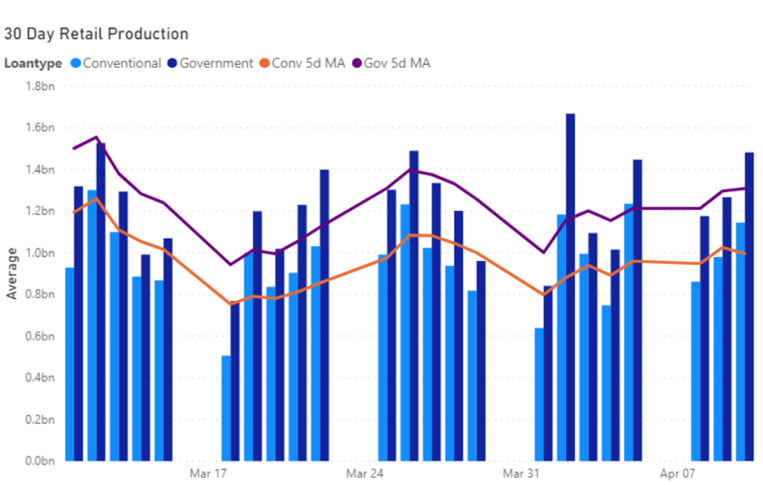

Per Black Knight's Production Metrics, the breakdown of mortgage production volume is as follows: 84.79% for purchase transactions, 10.81% for cash-out refinances, and 4.40% for rate and term refinances.

Per Black Knight 50.78% of all Retail loan production were Government Loans (FHA, VA, USDA), while 49.20% were Conventional and Non-Conforming loans.

Interesting Fact:

Compared to the 2006 Housing Boom peak, home prices are currently 71% higher. However, after accounting for inflation, home prices are just 10% higher. Thought of slightly differently, nominal home prices are exactly double what they were in 2004. That works out to a compound annual growth rate of 3.6%. While housing prices went crazy during Covid, over the long run price increases have been rather pedestrian.

- Elliot F. Eisenberg, former Sr. Economist with National Association of Home Builders

News You Can Use:

- One Cut, Then Five, Then Two: Goldman’s Calls Roiled by CPI

- Inflation is sticking around. Here's what that means for interest rate cuts — and your money.

- Here's where U.S. homeowners pay the most — and least — in property taxes

- Traders See Fed Waiting Until After Summer to Cut as Yields Soar

- Building a luxury home in an expensive real estate market: 5 tips

- List of the 10 Metro Areas with Largest Share of Price Reductions of Total Inventory

*Communication is intended for Industry Professionals only and not intended for Consumer Distribution

Interest rate and annual percentage rate (APR) are based on current market conditions as of 04/10/2024, are for informational purposes only, are subject to change without notice and may be subject to pricing add-ons related to property type, loan amount, loan-to-value, credit score and other variables. Estimated closing costs used in the APR calculation are assumed to be paid by the borrower at closing. If the closing costs are financed, the loan, APR and payment amounts will be higher. Contact us for details. Additional loan programs may be available. Accuracy is not guaranteed, and all products may not be available in all borrower's geographical areas and are based on their individual situation. This is not a credit decision or a commitment to lend. actual interest rate, APR, and payment may vary based on the specific terms of the loan selected, verification of information, your credit history, the location and type of property, and other factors as determined by Prosperity Home Mortgage, LLC. Not available in all states. Rate is as of 04/10/2024 and is subject to change at any time without notice. Opinions, estimates, forecasts, and other views contained in this document are those of Freddie Mac's economists and other researchers, do not necessarily represent the views of Freddie Mac or its management, and should not be construed as indicating Freddie Mac's business prospects or expected results. Although the authors attempt to provide reliable, useful information, they do not guarantee that the information or other content in this document is accurate, current, or suitable for any particular purpose. All content is subject to change without notice. All content is provided on an "as is" basis, with no warranties of any kind whatsoever. Information from this document may be used with proper attribution.

All first mortgage products are provided by Prosperity Home Mortgage, LLC. (877) 275-1762. Prosperity Home Mortgage, LLC products may not be available in all areas. Not all borrowers will qualify. Licensed by the Department of Financial Protection and Innovation under the California Residential Mortgage Lending Act. Licensed by the Delaware State Bank Commissioner. Massachusetts Mortgage Lender License ML75164. Licensed by the NJ Department of Banking and Insurance. Licensed Mortgage Banker-NYS Department of Financial Services. Also licensed in AK, AL, AR, AZ, CO, CT, DC, FL, GA, ID, IL, IN, KS, KY, LA, MD, ME, MI, MN, MO, MS, MT, NC, ND, NE, NH, NM, NV, OH, OK, OR, PA, RI, SC, SD, TN, TX, UT, VA, VT, WA, WI, WV and WY. NMLS ID #75164 (For licensing information go to: NMLS Consumer Access at http://www.nmlsconsumeraccess.org/)