This Market Update is written by our Capital Market specialists each week to bring you insight into what's happening in the market and how it may affect mortgage rates and real estate trends.

Market Commentary:

For the week of Jan 12th – Jan 18th, 30-year and 15-year interest rates increased slightly.

While rates remain elevated this week, the Fed recently signaled that it would begin to cut rates in 2024, indicating a further downward shift in mortgage rates may be on the way.

Mortgage rates fell sharply in mid-December as the Federal Reserve wrapped up its final meeting of 2023 with no rate hike. The Fed did signal several rate cuts in 2024, and mortgage rates responded by free-falling from 7.21 percent to 6.88 percent in a single week.

A growing number of housing economists say mortgage rates could stay below 7 percent in the coming months. This is an encouraging development for the housing market and in particular first-time homebuyers who are sensitive to changes in housing affordability.

Fed Watch:

Looking ahead, all eyes are now on the upcoming January 31st, Federal Open Market Committee (FOMC) meeting. According to the CME Group, 0.00% of forecasters predict an increase in interest rates, while 97.4% predict rates will remain the same. 2.6% of forecasters expect rates to decrease.

Market Review:

Per Black Knight's Production Metrics, the breakdown of mortgage production volume is as follows: 84.16% for purchase transactions, 11.08% for cash-out refinances, and 4.77% for rate and term refinances.

Per Black Knight 49.33% of all Retail loan production were Government Loans (FHA, VA, USDA), while 50.67% were Conventional and Non-Conforming loans.

Key Housing-Market Data:

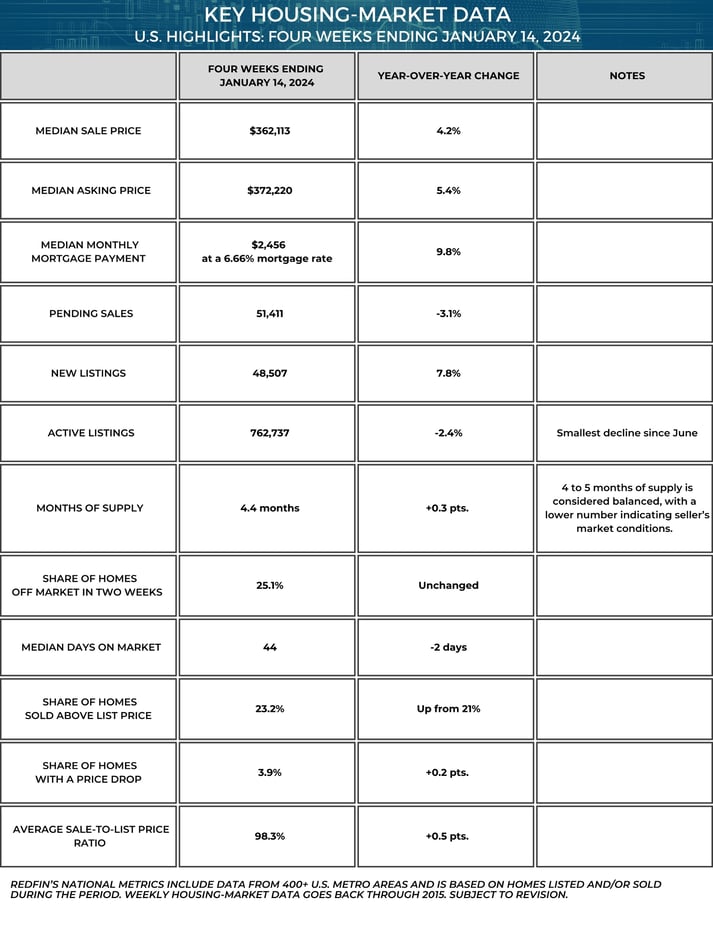

Homebuyers and sellers are gradually becoming more active as the calendar flips further into 2024. Mortgage-purchase applications are up 8% from a month ago, lower mortgage rates are piquing buyers’ interest. On the sell side, new listings increased 8% year over year during the four weeks ending January 14.

Buyers and sellers are making moves largely because mortgage rates are holding steady in the mid-6% range, down from 8% in October. The typical U.S. homebuyer’s monthly housing payment is $2,456 with this week’s average rate; while that’s up 10% year over year, it’s down from October’s record high of over $2,700.

News You Can Use:

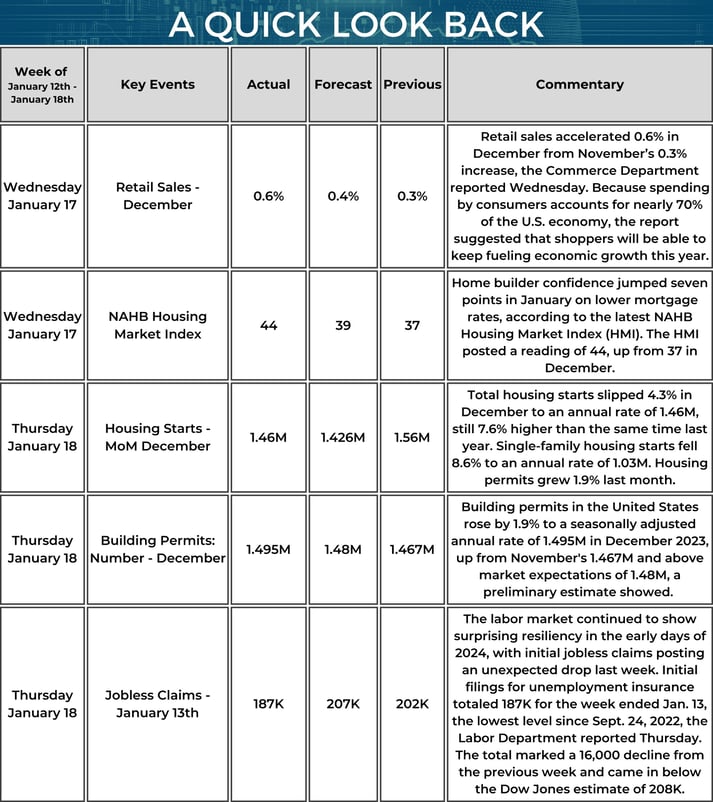

- Strong US retail sales underscore economy's momentum heading into 2024

- NAHB Housing Market Index: Builder Confidence Surges on Falling Interest Rates

- Weekly jobless claims post lowest reading since September 2022

- S. Mortgage Demand Jumps 10% as Rates Fall Across the Board

- Mortgage Rates Are Likely To Rise—but Here’s Why Homebuyers Shouldn’t Panic

- Remodeling Market Sentiment Improves in Fourth Quarter

*Communication is intended for Industry Professionals only and not intended for Consumer Distribution

Interest rate and annual percentage rate (APR) are based on current market conditions as of 01/11/2023, are for informational purposes only, are subject to change without notice and may be subject to pricing add-ons related to property type, loan amount, loan-to-value, credit score and other variables. Estimated closing costs used in the APR calculation are assumed to be paid by the borrower at closing. If the closing costs are financed, the loan, APR and payment amounts will be higher. Contact us for details. Additional loan programs may be available. Accuracy is not guaranteed, and all products may not be available in all borrower's geographical areas and are based on their individual situation. This is not a credit decision or a commitment to lend. actual interest rate, APR, and payment may vary based on the specific terms of the loan selected, verification of information, your credit history, the location and type of property, and other factors as determined by Prosperity Home Mortgage, LLC. Not available in all states. Rate is as of 01/11/2023 and is subject to change at any time without notice. Opinions, estimates, forecasts, and other views contained in this document are those of Freddie Mac's economists and other researchers, do not necessarily represent the views of Freddie Mac or its management, and should not be construed as indicating Freddie Mac's business prospects or expected results. Although the authors attempt to provide reliable, useful information, they do not guarantee that the information or other content in this document is accurate, current, or suitable for any particular purpose. All content is subject to change without notice. All content is provided on an "as is" basis, with no warranties of any kind whatsoever. Information from this document may be used with proper attribution.

All first mortgage products are provided by Prosperity Home Mortgage, LLC. (877) 275-1762. Prosperity Home Mortgage, LLC products may not be available in all areas. Not all borrowers will qualify. Licensed by the Department of Financial Protection and Innovation under the California Residential Mortgage Lending Act. Licensed by the Delaware State Bank Commissioner. Massachusetts Mortgage Lender License ML75164. Licensed by the NJ Department of Banking and Insurance. Licensed Mortgage Banker-NYS Department of Financial Services. Also licensed in AK, AL, AR, AZ, CO, CT, DC, FL, GA, ID, IL, IN, KS, KY, LA, MD, ME, MI, MN, MO, MS, MT, NC, ND, NE, NH, NM, NV, OH, OK, OR, PA, RI, SC, SD, TN, TX, UT, VA, VT, WA, WI, WV and WY. NMLS ID #75164 (For licensing information go to: NMLS Consumer Access at http://www.nmlsconsumeraccess.org/)