This Market Update is written by our Capital Market specialists each week to bring you insight into what's happening in the market and how it may affect mortgage rates and real estate trends.

Market Commentary:

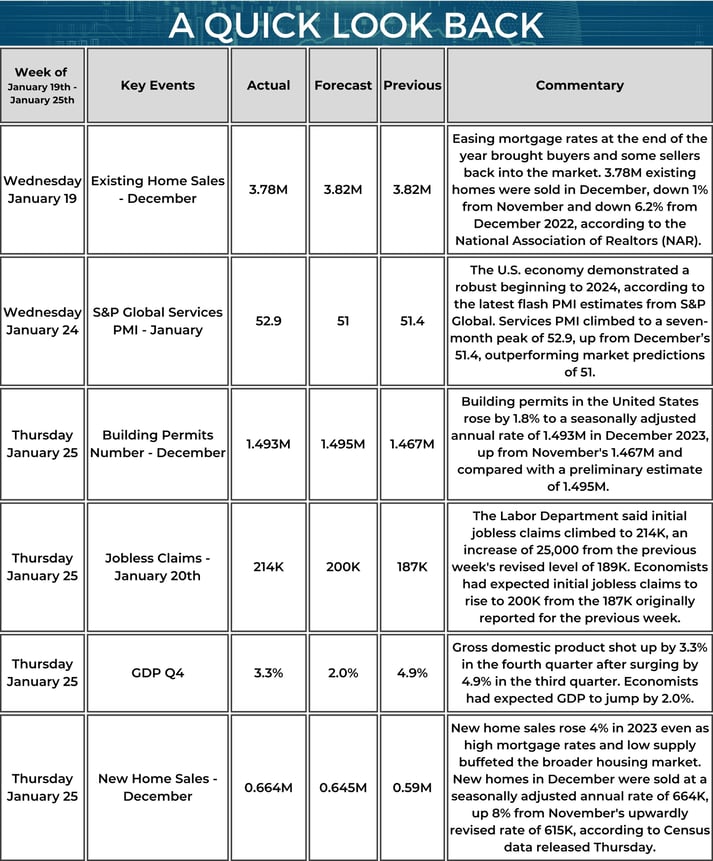

For the week of Jan 19th – Jan 25th, 30-year and 15-year interest rates remained steady. The 30-year fixed-rate has remained within a very narrow range over the last month. Given this stabilization in rates, potential homebuyers with affordability concerns have jumped off the fence and back into the market. Despite persistent inventory challenges, we anticipate a busier spring homebuying season than 2023, with home prices continuing to increase at a steady pace.

What affects mortgage rates?

Federal Reserve monetary policy: The nation’s central bank doesn’t set interest rates, but when it adjusts the federal funds rate, mortgages tend to go in the same direction.

Inflation: Mortgage rates tend to increase during high inflation. Lenders usually set higher interest rates on loans to compensate for the loss of purchasing power.

The bond market: Mortgage lenders often use long-term bond yields, like the 10-Year Treasury, as a benchmark to set interest rates on home loans. When yields rise, mortgage rates typically increase.

Geopolitical events: World events, such as elections, pandemics, or economic crises, can also affect home loan rates, particularly when global financial markets face uncertainty.

Other economic factors: The bond market, employment data, investor confidence, and housing market trends – such as supply and demand – can also affect the direction of mortgage rates.

Fannie Mae projects that rates will fall going into 2024 and throughout next year. Fannie Mae’s rate projections have decreased from 6.48% by the end of 2024 to a revised estimate of around 5.8% or lower as per the chart below:

Fed Watch:

Looking ahead, all eyes are now on the upcoming January 31st, Federal Open Market Committee (FOMC) meeting. According to the CME Group, 0.00% of forecasters predict an increase in interest rates, while 97.4% predict rates will remain the same. 2.6% of forecasters expect rates to decrease.

Market Review:

Per Black Knight's Production Metrics, the breakdown of mortgage production volume is as follows: 83.24% for purchase transactions, 12.16% for cash-out refinances, and 4.61% for rate and term refinances.

Per Black Knight 49.36% of all Retail loan production were Government Loans (FHA, VA, USDA), while 50.64% were Conventional and Non-Conforming loans.

News You Can Use:

- Fannie Mae: 2024 Mortgage Rates to Dip Below 6%

- Are happy days here again for mortgage industry?

- S. Economic Growth Far Exceeds Estimates In Q4

- Demand for mortgages picks up: MBA

- US new home sales up in 2023, boosted by limited existing supply

- US dollar up slightly after GDP data

*Communication is intended for Industry Professionals only and not intended for Consumer Distribution

Interest rate and annual percentage rate (APR) are based on current market conditions as of 01/26/2024, are for informational purposes only, are subject to change without notice and may be subject to pricing add-ons related to property type, loan amount, loan-to-value, credit score and other variables. Estimated closing costs used in the APR calculation are assumed to be paid by the borrower at closing. If the closing costs are financed, the loan, APR and payment amounts will be higher. Contact us for details. Additional loan programs may be available. Accuracy is not guaranteed, and all products may not be available in all borrower's geographical areas and are based on their individual situation. This is not a credit decision or a commitment to lend. actual interest rate, APR, and payment may vary based on the specific terms of the loan selected, verification of information, your credit history, the location and type of property, and other factors as determined by Prosperity Home Mortgage, LLC. Not available in all states. Rate is as of 01/26/2024 and is subject to change at any time without notice. Opinions, estimates, forecasts, and other views contained in this document are those of Freddie Mac's economists and other researchers, do not necessarily represent the views of Freddie Mac or its management, and should not be construed as indicating Freddie Mac's business prospects or expected results. Although the authors attempt to provide reliable, useful information, they do not guarantee that the information or other content in this document is accurate, current, or suitable for any particular purpose. All content is subject to change without notice. All content is provided on an "as is" basis, with no warranties of any kind whatsoever. Information from this document may be used with proper attribution.

All first mortgage products are provided by Prosperity Home Mortgage, LLC. (877) 275-1762. Prosperity Home Mortgage, LLC products may not be available in all areas. Not all borrowers will qualify. Licensed by the Department of Financial Protection and Innovation under the California Residential Mortgage Lending Act. Licensed by the Delaware State Bank Commissioner. Massachusetts Mortgage Lender License ML75164. Licensed by the NJ Department of Banking and Insurance. Licensed Mortgage Banker-NYS Department of Financial Services. Also licensed in AK, AL, AR, AZ, CO, CT, DC, FL, GA, ID, IL, IN, KS, KY, LA, MD, ME, MI, MN, MO, MS, MT, NC, ND, NE, NH, NM, NV, OH, OK, OR, PA, RI, SC, SD, TN, TX, UT, VA, VT, WA, WI, WV and WY. NMLS ID #75164 (For licensing information go to: NMLS Consumer Access at http://www.nmlsconsumeraccess.org/)