This Market Update is written by our Capital Market specialists each week to bring you insight into what's happening in the market and how it may affect mortgage rates and real estate trends.

Rates are provided by Mortgage News Daily. The MND Rate Index is the best way to follow day-to-day movement in mortgage rates. The index is driven by real-time changes in actual lender rate sheets. This has two huge advantages, timeliness and accuracy. A "top tier" scenario is used as a baseline (75LTV, 780 FICO, etc.). We use proprietary methodology to adjust the rate to account for points. That can mean that lenders are quoting 6.125 with points while our index is at 6.25, hypothetically.

Market Commentary:

Mortgage rates broke below 6% this week for the first time since 2022, marking a major turning point for buyers and sellers heading into the spring market. The average 30‑year fixed rate fell to 5.98% a three‑year low unlocking meaningful affordability gains and easing the lock‑in effect that has kept inventory tight. With rates stabilizing under 6% and buyer sentiment improving, both demand and new listings are expected to strengthen as we move into March.

The rate decline is already reshaping expectations for the spring 2026 market. Inventory pressure may ease. Lower rates reduce the “lock‑in effect,” encouraging homeowners with ultra‑low pandemic‑era mortgages to consider listing. Buyer activity is thawing. Pent‑up demand from 2024–2025 is re‑emerging as affordability improves. Affordability improves meaningfully. Even a 0.25–0.50% rate drop can restore purchasing power, especially in high‑cost markets. Market sentiment is shifting. Analysts describe this as the first real “thaw” after years of rate‑driven stagnation.

FedWatch: Target rate (in bps) possibilities, according to the CME Group (as of 03/05/2026 – 12:00 PM EST):

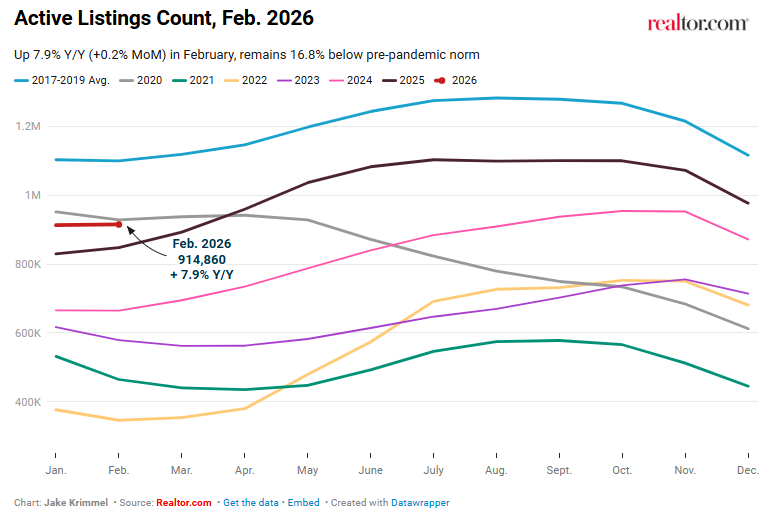

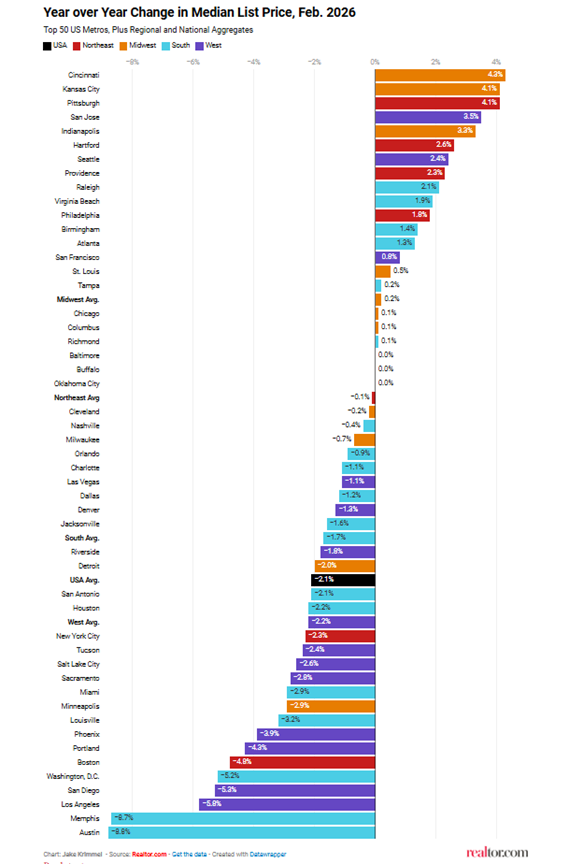

February 2026 Monthly Housing Report: Inventory Rises as Prices Edge Down:

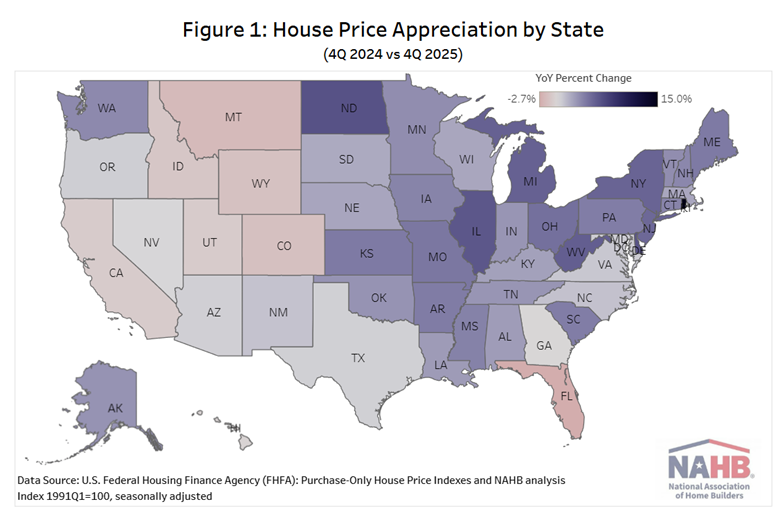

House Price Appreciation by State and Metro Area: Fourth Quarter 2025:

The Typical U.S. Homeowner Hangs Onto Their House For 12 Years, the longest median tenure since2022. In Los Angeles, It’s 20 Years.

Deepening Delinquency:

In 25Q4, the aggregate delinquency rate across all debt types was 4.8%,up from 4.5% Q-o-Q. This is the ninth quarterly increase in the past 10 quarters. The rate bottomed out in 22Q4 at about 2.5%. More significantly, the rate is back where it was before Covid, but it’s still rising and may soon approach a 10-year high. The rate is up significantly for student loans and slightly for mortgages. - Elliot Eisenberg, Economist

News You Can Use:

· Weekly mortgage demand surged 11% higher last week, as rates sat near 4-year low.

· Mortgage Rates Move Back Down Despite Stronger Data

· Trump officially nominates Kevin Warsh as Federal chair

· Big investors exiting for-sale housing market, even before Trump ban

· Private companies added 63,000 jobs in February, January revised to just 11,000 additions, ADP says

· The 5 Strongest States Leading the '2-Speed' Housing Market

*Communication is intended for Industry Professionals only and not intended for Consumer Distribution

Interest rate and annual percentage rate (APR) are based on current market conditions as of 03/05/2026, are for informational purposes only, are subject to change without notice and may be subject to pricing add-ons related to property type, loan amount, loan-to-value, credit score and other variables. Estimated closing costs used in the APR calculation are assumed to be paid by the borrower at closing. If the closing costs are financed, the loan, APR and payment amounts will be higher. Contact us for details. Additional loan programs may be available. Accuracy is not guaranteed, and all products may not be available in all borrower's geographical areas and are based on their individual situation. This is not a credit decision or a commitment to lend. actual interest rate, APR, and payment may vary based on the specific terms of the loan selected, verification of information, your credit history, the location and type of property, and other factors as determined by Prosperity Home Mortgage, LLC. Not available in all states. Rate is as of 03/05/2026 and is subject to change at any time without notice. Opinions, estimates, forecasts, and other views contained in this document are those of Freddie Mac’s economists and other researchers, do not necessarily represent the views of Freddie Mac or its management, and should not be construed as indicating Freddie Mac’s business prospects or expected results. Although the authors attempt to provide reliable, useful information, they do not guarantee that the information or other content in this document is accurate, current, or suitable for any particular purpose. All content is subject to change without notice. All content is provided on an “as is” basis, with no warranties of any kind whatsoever. Information from this document may be used with proper attribution.