This Market Update is written by our Capital Market specialists each week to bring you insight into what's happening in the market and how it may affect mortgage rates and real estate trends.

Market Commentary:

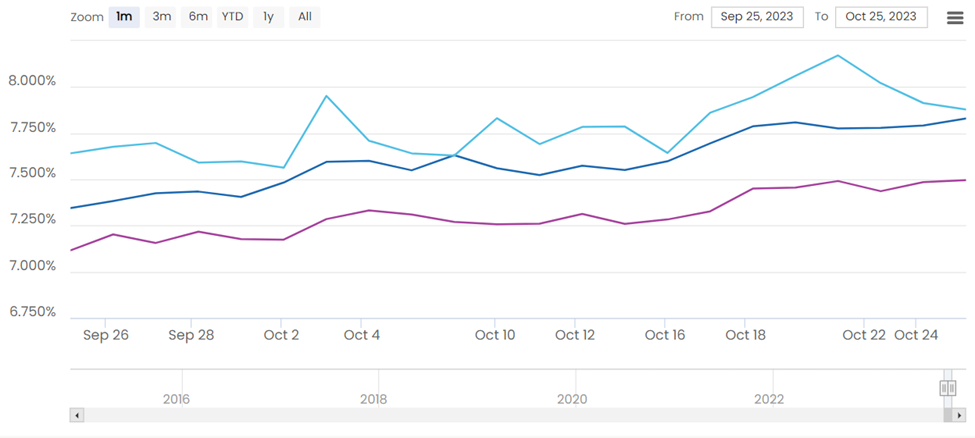

For the week of Oct 20th – Oct 26th, 30-year and 15-year interest rates increased.

Mortgage rates are up only a few basis points compared to where they were last week. That said, rates are expected to fall throughout the next couple of years, but it could take a while before we see a substantial improvement in affordability. In their latest forecast, Fannie Mae researchers predicted that rates would drop to 6.7% by the end of 2024.

Housing Market Predictions for Winter 2023

-

Home prices and mortgage rates are both expected to remain high this winter, keeping the market challenging for buyers.

-

The housing shortage may improve slightly, but overall, the lack of inventory is expected to persist.

-

Even so, experts say if you are financially prepared for a home purchase, don't let the market conditions stop you.

-

The median price of new houses sold was $418,800, while the average sales price was $503,900, as opposed to $477,700 and $530,100 respectively a year ago. At the end of September, there were 435K houses remaining for sale, equivalent to a 6.9-month supply at the current sales rate.

Fed Watch: Looking ahead, all eyes are now on the upcoming November 1st Federal Open Market Committee (FOMC) meeting. According to the CME Group, 1.8% of forecasters predict an increase in interest rates, while 98.2% predict rates will remain the same. None of the forecasters expect rates to decrease.

Market Review:

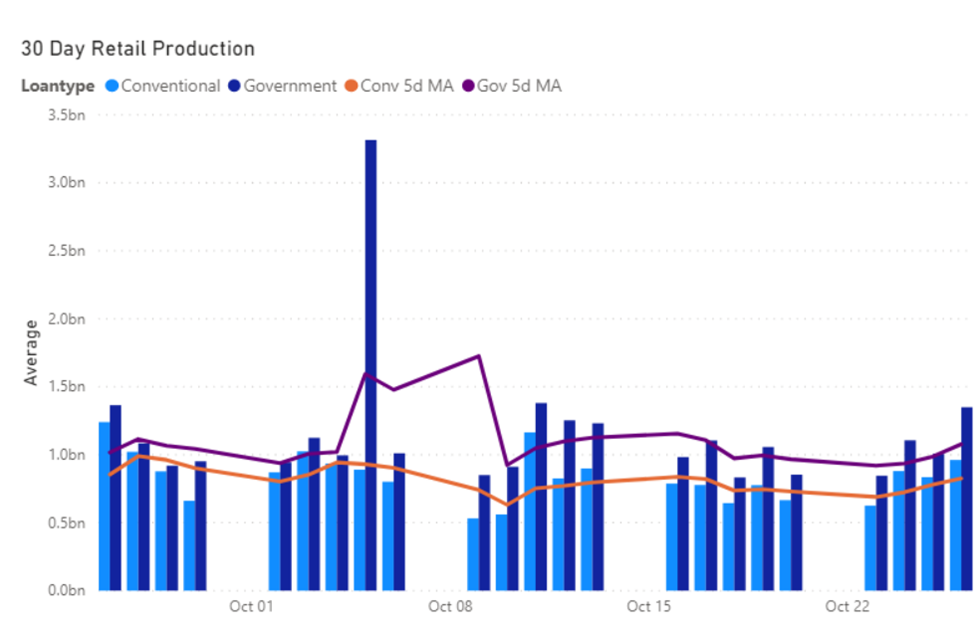

Per Black Knight's Production Metrics, the breakdown of mortgage production volume is as follows: 86.14% for purchase transactions, 11.69% for cash-out refinances, and 2.17% for rate and term refinances.

Per Black Knight 51.88% of all Retail loan production were Government Loans (FHA, VA, USDA), while 48.22% were Conventional and Non-Conforming loans.

News You Can Use:

- US economy grows at fastest pace in nearly two years

- Winning the Bid: The Cities Where Homebuyers Are Making the Largest—and Smallest—Down Payments

- Housing market predictions: Don’t expect home prices to come down, Goldman Sachs says

- What Is a Barndominium? The Hottest New Home Trend, Explained

- Pending home sales rose in September, despite high mortgage rates

*Communication is intended for Industry Professionals only and not intended for Consumer Distribution

Interest rate and annual percentage rate (APR) are based on current market conditions as of 10/27/2023, are for informational purposes only, are subject to change without notice and may be subject to pricing add-ons related to property type, loan amount, loan-to-value, credit score and other variables. Estimated closing costs used in the APR calculation are assumed to be paid by the borrower at closing. If the closing costs are financed, the loan, APR and payment amounts will be higher. Contact us for details. Additional loan programs may be available. Accuracy is not guaranteed, and all products may not be available in all borrower's geographical areas and are based on their individual situation. This is not a credit decision or a commitment to lend. actual interest rate, APR, and payment may vary based on the specific terms of the loan selected, verification of information, your credit history, the location and type of property, and other factors as determined by Prosperity Home Mortgage, LLC. Not available in all states. Rate is as of 10/27/2023 and is subject to change at any time without notice. Opinions, estimates, forecasts, and other views contained in this document are those of Freddie Mac's economists and other researchers, do not necessarily represent the views of Freddie Mac or its management, and should not be construed as indicating Freddie Mac's business prospects or expected results. Although the authors attempt to provide reliable, useful information, they do not guarantee that the information or other content in this document is accurate, current, or suitable for any particular purpose. All content is subject to change without notice. All content is provided on an "as is" basis, with no warranties of any kind whatsoever. Information from this document may be used with proper attribution.